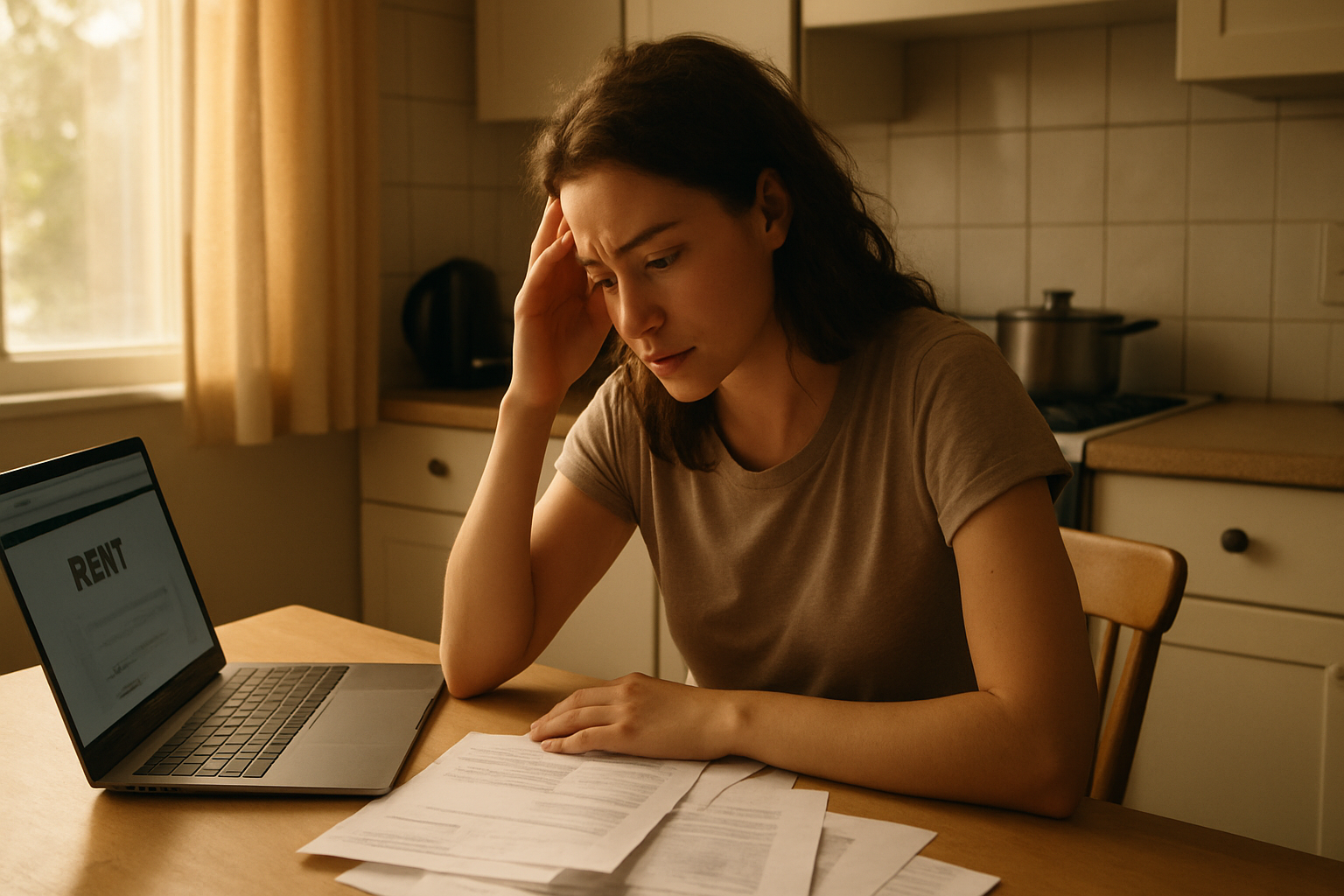

A new wave of financial products is quietly spreading through the U.S. rental market: rent now pay later loans that let tenants split their monthly rent into smaller installments — often with steep fees and interest rates attached. The Financial Times reported the trend in depth, finding that fintech startups and established lenders alike are racing to capture millions of Americans who can no longer comfortably cover rent in a single payment.

The non-obvious detail buried in the story: some of these products don’t report payments to credit bureaus when things go well — but do report when borrowers default. That asymmetry means renters build no credit benefit from on-time payments, yet face a credit score hit the moment they fall behind.

How Rent Now Pay Later Products Actually Work

The basic model borrows heavily from the buy now pay later playbook made popular by companies like Affirm and Klarna in retail shopping. A third-party lender pays the landlord the full month’s rent upfront. The tenant then repays the lender in two or four installments over the month, plus a flat fee or annualized interest that can range from 15% to well over 100% APR depending on the provider and the borrower’s risk profile.

Some platforms market themselves directly to property management companies, which embed the option into their tenant payment portals. Others operate as standalone apps renters download independently. Either way, the landlord gets paid on time and the financial risk shifts entirely to the borrower.

Housing costs remain the single largest line item in most American household budgets. Median asking rents in major metro areas have climbed sharply over the past several years, and while rent growth has cooled slightly in some Sun Belt cities in 2026, affordability remains severely strained. The U.S. Census Bureau tracks millions of renter households as “cost-burdened,” meaning they spend more than 30% of gross income on housing.

Who Is Taking On Rental Debt — and Why

The target customer for rent now pay later lenders is not someone in acute financial crisis. Marketers pitch the product to working renters whose paychecks and rent due dates simply don’t align — people paid biweekly who face a rent bill on the first of the month before their next direct deposit clears. That’s a real and widespread cash-flow problem, and lenders are leaning into it hard.

But consumer advocates warn the framing obscures the true cost. A $20 flat fee on a $1,500 rent payment sounds modest. Spread over two weeks, that annualizes to nearly 35% APR. On shorter repayment windows or larger fees, the effective rate climbs much faster. Unlike a traditional personal loan, these products often aren’t subject to the same disclosure requirements, making side-by-side comparisons difficult for borrowers.

There’s also a debt spiral risk that critics flag loudly. A renter who relies on an installment product one month is statistically more likely to need it again the next — each time paying fees that further compress an already tight budget. That dynamic is well-documented in the payday lending literature, and housing advocates worry rent now pay later is simply repackaging the same cycle in a more respectable wrapper.

The Regulatory Gray Zone

Federal oversight of these products is fragmented. Some fall under the Truth in Lending Act if they charge interest; others are structured as “fees” to sidestep that classification. The Consumer Financial Protection Bureau has signaled interest in the broader buy now pay later space, but specific rent-focused rules remain thin as of mid-2026.

Several states have moved faster. California and New York have proposed legislation requiring standardized APR disclosures on any installment product tied to housing payments. Critics of those proposals argue overly strict rules could push the products out of the market entirely, leaving cash-strapped renters with worse options — payday loans, overdraft fees, or late-payment penalties from landlords that can also be financially punishing.

The debate mirrors earlier fights over buy now pay later regulation in retail, though the stakes feel higher when the product being financed is someone’s home rather than a pair of sneakers. For more on how consumer lending decisions are playing out in other high-stakes arenas, see our coverage of Utah residents suing officials over a major financial development deal — another case where everyday people pushed back against powerful financial actors.

What Renters Should Watch For

- APR, not just fees. Always ask for the annualized rate, even if the lender only advertises a flat dollar amount.

- Credit reporting terms. Find out whether on-time payments are reported to any bureau — if they’re not, you’re getting none of the upside.

- Landlord relationships. Some lease agreements treat third-party payments as a violation. Check your lease before signing up.

- Exit ramp. Understand what happens if you miss an installment — late fees, collections referrals, and lease consequences can compound fast.

What Comes Next

Fintech investment in the rent payment space has accelerated through the first half of 2026, with several startups closing Series B rounds and at least one major bank-backed platform announcing a national rollout. Regulatory pressure is building in parallel, and the CFPB is expected to publish new guidance on installment products tied to essential expenses before the end of the year.

For renters who feel squeezed by housing costs, the appeal of splitting a $2,000 rent bill into manageable chunks is completely understandable. The question is whether the fine print turns a short-term cash-flow fix into a longer-term financial hole — and right now, that answer depends heavily on which product a renter happens to find first.

The housing affordability crisis driving demand for these loans shows no sign of resolving quickly. As the FT’s reporting makes clear, rent now pay later is filling a genuine gap — but gaps filled by high-cost credit have a history of widening the problems they claim to solve. Staying informed about consumer lending and housing affordability efforts is more important than ever for renters navigating this landscape.